“We will see $300 a barrel — or roughly $250 in today’s dollars — because oil supply will be so short. If you want that oil, that’s what you will have to pay for it. That will be in 2015, after the peak of oil [supply].”

Charles Maxwell, a well-known analyst at Weeden & Co., made that prediction in 2008 (see the Barron’s article, What $300-a-Barrel Oil Will Mean for You). Three years later, he stayed with his $300-a-barrel prediction, but shifted the timeframe to 2020 (see the CBS News article, Another $300 Oil Prediction — and Why This One Matters).

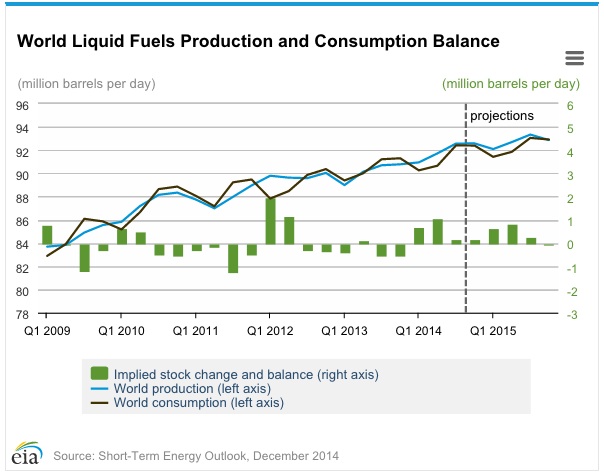

2015 is less than three weeks away, and a barrel of Brent crude oil is $65.70 as of this morning — a lower price than 5 years ago!

I use this example to illustrate the challenges (or, perhaps, the futility) of making supply chain and logistics predictions. In many cases, we look at recent trends and simply project them forward, but this assumes that the factors impacting that trend, either directly or indirectly, will remain the same, which is often a false assumption. In the case of oil, for example, the rise of shale oil production, especially in the United States, has significantly increased supply, which has put downward pressure on prices and has stirred up the debate again about “peak oil” predictions. The EIA now expects that “global liquid fuels supply will continue to outpace consumption, resulting in an average stock build of 0.4 million bbl/d in 2015.”

In other cases, as the saying goes, we simply fail to see the forest for the trees when making predictions. When I worked at Polaroid, for example, some of us were concerned about the emergence of digital cameras and what it would do to instant photography. We never expected or predicted that the clunky analog cell phones we carried on our belt clips back then would quickly evolve into Internet-connected smartphones with digital cameras built-in, which is today cannibalizing digital camera sales!

Simply put, I admit upfront that my supply chain and logistics predictions below are biased and flawed, but I make them anyway because it’s a fun exercise, and also because I hope it generates some thoughtful conversations and ideas.

I limited myself to just six predictions, although I believe many of the predictions I made last year (and the year before that) will continue to play out in 2015 and beyond, so I encourage you to revisit those predictions too (I listed them below for quick reference).

As the American computer scientist Alan Kay famously said, “The best way to predict the future is to invent it.” So, here is my invented future for 2015, starting with my most audacious prediction:

Google will acquire a logistics service provider (3PL) and/or a logistics software vendor.

It’s no secret that Google and Amazon.com are continuously looking to outmaneuver each other, especially in logistics-related areas such as same-day delivery and drones. But as I wrote back in April 2013, “If you look closely, Amazon’s real advantage comes from its logistics assets — the 89 distribution centers it [had at the time], including 20 opened [in 2012], with more scheduled to open in the months ahead. And its technology assets too, like the Kiva robots Amazon purchased [in 2012] and the data centers that power its cloud computing services. What’s even more interesting…is that Amazon is leveraging these assets to provide fulfillment services for other companies.”

In short, logistics is becoming a greater competitive differentiator for companies across all industries, so if Google wants to seriously compete with Amazon on that front, it needs to become a 3PL, and enhance its logistics software and technology capabilities too.

For related commentary, see:

- In Logistics, Somebody Has to Own the Assets

- Amazon Inside P&G Warehouses: A Case of “What’s In It for We”

- Do Facebook and Twitter Need a Logistics Strategy?

- The Google TMS?

- The Google Robot, Your Future Logistics Worker

More companies will treat Supply Chain Design as a continuous business process instead of a standalone project or a once-a-year exercise.

Historically, Supply Chain Design was an exercise companies undertook at most once a year, or when a significant change occurred in their supply chain, such as an acquisition. It was a strategic/tactical analysis, disconnected from day-to-day operations, and the software tools were difficult to learn and use.

Today, Supply Chain Design is becoming more operational and real-time, as companies have to respond more quickly and intelligently to fast-changing forces impacting their business (e.g., competitive threats, new regulations, more stringent customer expectations). Best-in-class companies are either developing Supply Chain Design competency in-house or expecting it from their logistics service providers, and they are using the technology (which is more user-friendly and affordable than in the past) on a more frequent and consistent basis for Product Flowpath Analysis, Cost-to-Serve Optimization, Safety Stock Optimization, Tax/Duties Optimization, and Risk Management (among other things).

For related commentary, see Insights from Ryder Innovate 2014.

3PLs and software vendors will focus more on acquiring small and midsize customers, and on serving the needs of companies in the Energy and Process Industries.

For a variety of reasons (the high cost of sales being one of them), most 3PLs and software vendors have historically underserved the SMB market, focusing their sales efforts on large companies instead. But as the top end of the market becomes more saturated and competitive — and as new competitors emerge with hybrid business models, offering customers more flexible, faster-to-deploy, and more cost-effective solutions — the race is on to win market share in the SMB market, and to do so profitably.

A similar race is on to expand beyond the usual set of industries — namely, Automotive, High Tech, Retail, and CPG — and establish a leading presence in historically underserved and underpenetrated vertical industries, such as Oil & Gas and Chemical. Generally speaking, companies in the Energy and Process Industries are lower on the supply chain maturity curve than companies in Automotive and High Tech, but they face significant supply chain challenges and opportunities nonetheless — and more importantly, they are now motivated to move up the maturity curve (that is, invest in technology and pursue outsourcing relationships) as cost pressures, competitive forces, regulatory requirements, and customer expectations intensify.

For related commentary, see:

- Notable Quote: C.H. Robinson Acquires Freightquote

- Managed Services: The “Stretch Armstrong” of Logistics

- Process Industry Moving Up the Supply Chain Maturity Curve

- Big Data and Analytics for Oil and Gas Transportation

- 3PLs Need to Take Broader Perspective

Companies will begin to transform their decision-making processes, which will lead to greater use of social networking technologies.

As noted earlier, in order to keep pace with the rapid pace of change, companies need to make smarter decisions faster. It’s the promise of Big Data, Business Intelligence, and Analytics. But those technologies are worthless if companies don’t also transform and accelerate their decision-making processes. At many companies, decisions get bogged down by months of testing and review (“analysis paralysis”), endless internal debates, the pursuit of consensus (to cover everybody’s ass in case something goes wrong), and the weight of giant teams. To overcome these issues, companies will have to change their decision-making processes and “walk the talk” on empowering individuals and teams to make decisions. They will also have to embrace social networking tools to enable employees and external trading partners to communicate, collaborate, and execute business processes in more efficient, scalable, and innovative ways.

For related commentary, see:

- Transform Your Decision-Making Process

- Facebook for Supply Chain Communication and Collaboration?

- HP’s New Style of IT: The Social Supply Chain

- Want a Fast-Response Supply Chain? Facilitate People-to-People Communication

Competitive threats, for both 3PLs and their customers, will cause them to transform the way they work together — that is, they will take a more Vested approach.

At an MIT conference last year, Tom Linton, Chief Procurement and Supply Chain Officer at Flextronics, presented his top 10 list of supply chain trends. Number one on his list was “‘Non-Zero’ Supply Chains Win.” In other words, supply chains focused on greater collaboration between everyone in the ecosystem will win. There is plenty of research by Nobel Prize winners and books by leading academics demonstrating the benefits of collaboration and taking a “What’s In It for We” approach to working with business partners. But to achieve those benefits, you have to take the first step: choose trust and see where it takes you.

For related commentary, see:

- Vested: How P&G, McDonald’s, and Microsoft are Redefining Winning in Business Relationships

- Develop a Shared Vision Statement with Your 3PL

- Apple: Still a Penny Wise and Pound Foolish?

- Time for a New RFP

- Perverse Incentives in Outsourcing Agreements

- Collaborate? Sure, Except I Don’t Trust You

The Great Unlearning Begins

The near-infinite processing power Cloud computing provides (along with other technological innovations) will cause everyone in the supply chain and logistics field to unlearn the way we’ve always done things, everything from the way we design software applications to how we design and manage supply chain processes. Simply put, what was once impossible or impractical due to computing power constraints, is now possible, at least technologically. The great unlearning process, however, won’t be quick or easy.

For related commentary, see A Case Study in Closed-Loop Operational Management.

What do you think of my predictions? What are your predictions for the coming year? Post a comment and share your perspective!

Also, join me next Tuesday, December 16 at 12:00 p.m. ET for a special episode of Talking Logistics where I will discuss my predictions in more detail, and you can ask me questions and participate in the conversation too.

—

Adrian’s Supply Chain and Logistics Predictions for 2014

- Shipping and delivery capabilities become even bigger competitive weapons.

- Shippers and carriers continue to shift away from long-haul trucking and one-way freight.

- Supply Chain Operating Networks (SCONs) introduce enhanced network-based analytics and social networking capabilities.

- Further “consumerization” of business IT.

- With operational excellence a given, IT and talent become greater value propositions for 3PLs.

- The robots keep coming.

- Energy will play a bigger role in supply chain strategies and decisions.

- Companies will become more proactive and smarter about supply chain risk management.

- Trade agreements, protectionism, and threat of port strike will dominate global trade news in first half of 2014.

Adrian’s Supply Chain and Logistics Predictions for 2013

- Big Data, Social Media, Cloud Computing, and Mobile will continue to dominate the headlines.

- Enterprise software user interfaces get a social media makeover

- “Siri” for enterprise apps.

- The robots keep coming.

- Innovating the final mile.

- Further blurring of the lines between 3PLs, technology providers, and consultants.

- Increased adoption of alternative fuel vehicles.

- More partnerships and programs to address talent shortage problem.