Editor’s Note: The following is an excerpt from “Network-based TMS: How Connected Platforms Will Transform Transportation Management in 2020 and Beyond,” a research e-book produced by Adelante SCM and published by Kuebix (a Talking Logistics sponsor).

No doubt, the current challenges in the transportation market are an acute response to an unexpected crisis [the COVID-19 pandemic]. However, the challenges are compounded by an ever-present truth in the industry: there’s a lot of waste in the system.

Empty miles — also referred to as “deadhead” or non-revenue miles — has been a longstanding problem in the trucking industry. According to research published by Convoy in August 2019:

Survey results from the late 1990s and early 2000s put empty miles between 15 percent and 18 percent. But there appears to have been no sharp improvements since then: Surveys from the past half-decade also put empty miles in the range of 15 percent to 20 percent.

In 2018, according to the American Transportation Research Institute, trucking companies accrued over 10 billion total operating miles; 16.6% of them were empty miles. With an overall cost per mile of $1.82, trucking companies spent $3.02 billion driving empty miles in 2018.

For private fleets, empty miles are a missed revenue opportunity. According to the National Private Truck Council and its 2019 Benchmarking Survey, 28% of private fleet empty miles were available for backhauls in 2019, with 50% of those empty miles available ‘for sale’ to others. Considering that the typical revenue per mile fleets realized in 2019 from backhauls was $1.86, that’s a lot of money being left on the table.

On the freight broker side, matching loads with available capacity has historically been a very time-consuming and labor-intensive process, often involving many phone calls and emails with shippers and carriers. This inefficiency limits the number of loads a broker can execute per day, which limits their ability to profitably grow their business without adding a lot more people. In addition, the vast majority of brokered loads have traditionally been one-offs — that is, a single pickup and delivery. Once the carrier completes the delivery, it has to find another load to move, triggering another cycle of phone calls and emails. In short, brokers have historically been unable to quickly and efficiently identify and book continuous moves for carriers, which leads to more empty miles for carriers and more wasted time and labor for brokers.

When it comes to shippers, their goal is to have access to capacity when they need it, at a competitive price, that meets their service-level expectations — or, more accurately, the service-level expectations of their customers. In the consumer goods industry, for example, “with expectations of higher on-shelf availability and lower inventory costs, the pressure on delivery performance has intensified—as has the need for manufacturers, retailers, and carriers to work together to create efficient, reliable, and responsive supply chains,” state the authors of a McKinsey & Company article. They go on to say:

In its effort to optimize its supply chains, the consumer industry has evolved in the way it measures delivery performance, moving away from the traditional “case-fill rate” and adopting the more rigorous “on-time in-full” (OTIF) delivery metric. OTIF measures the extent to which shipments are delivered to their destination according to both the quantity and schedule specified on the order. In theory, OTIF should be the ideal mechanism to align the objectives of retailers and manufacturers.

The vast majority of shipments are executed with contracted carriers — that is, with carriers that are part of a routing guide with negotiated rates and volume commitments. However, since transportation contracts are non-binding, a carrier can reject a load tender for a variety of reasons. Tender rejection rates vary over time based on market conditions, but they tend to average around 20% over the long term.

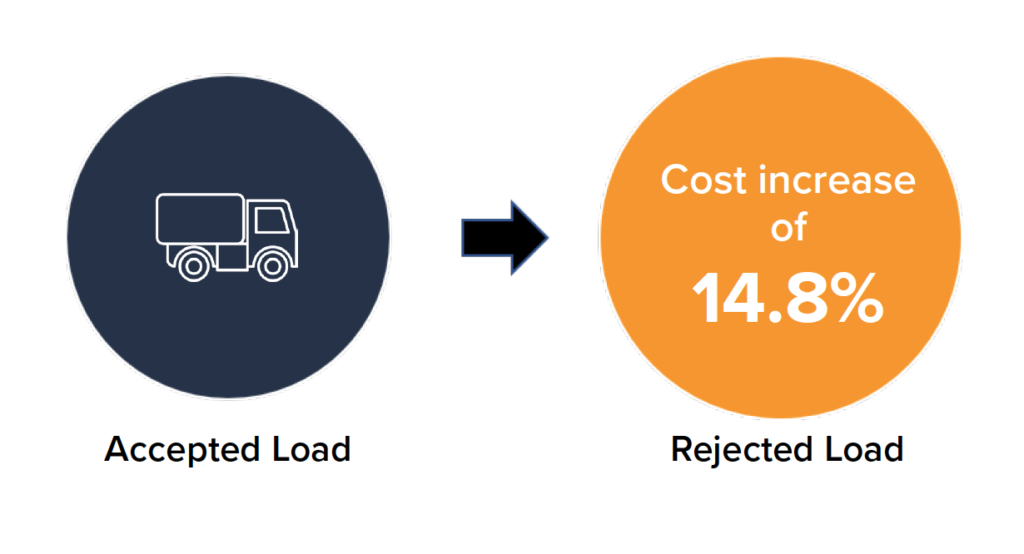

For example, based on a research study conducted by Yoo Joon Kim at MIT in 2013, “during the five years of the data period, the average rejection rate was 19.8%. When a load was rejected, the truckload price for the load increased by 14.8% on average. Due to the rejections, the shippers’ overall transportation expenditure increased by 2.8% on average.”

So, what happens when all contracted carriers in a routing guide reject a load? Many shippers still “dial for diesels” — that is, they pick up the phone and call a bunch of carriers to see who can pick up the load. Others manually post their loads on load boards and wait to see if a match occurs. Needless to say, these approaches are highly inefficient and costly.

Clearly, in light of all of this waste and inefficiency faced by all stakeholders in the transportation industry, coupled with more stringent customer service level requirements, the time has come to find a better and smarter way.

Network-based transportation management systems, and the network effects enabled by platforms that connect all logistics stakeholders, are the foundation for this required transformation.

For additional details about network-based transportation management systems, along with examples of the value created by the network effect in transportation, please download the research e-book, “Network-based TMS: How Connected Platforms Will Transform Transportation Management in 2020 and Beyond.”